Fantastic Journal Entry For Prepaid Salary Simple Profit And Loss Account Format

Prepaid Expenses Journal Entry How To Record Prepaids

The journal entry to record the hourly payrolls wages and withholdings for the work period of December 1824 is illustrated in Hourly Payroll Entry 1. Adjusting journal entry as the prepaid rent expires. Income must be recorded in the accounting period in which it is earned. Prepaid expense ac and expense ac. Prepaid insurance is insurance paid in advance and that has not yet expired on the date of the balance sheet Balance Sheet The balance. Cash paid to create the Prepaid Expense. 5000 Prepaid salary is debited because we have paid in advance so it is our asset and assets have dr balance. To do this debit your Expense account and credit your Prepaid Expense account. Prepaid expenses are payments made in advance resulting into a right to receive compensation or a claim to use assets of another entity like prepaid insurance and prepaid rent. The journal entries for prepaid rent are as follows.

The journal entry for prepaid expenses involves two accounts.

The journal entry would be as follows. These are expenses but taken as an asset because the benefit from them is still due. Prepaid insurance is insurance paid in advance and that has not yet expired on the date of the balance sheet Balance Sheet The balance. Prepaid expense ac and expense ac. Your journal entry reflecting the actual expense should look like this. Salaried Payroll Entry 1.

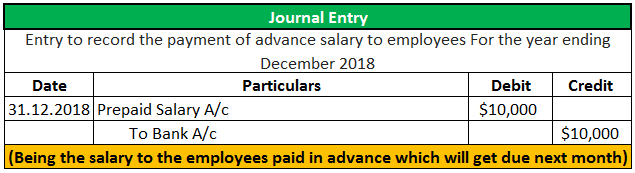

Adjusting journal entry as the prepaid rent expires. For example you have paid one month advance rent of your business shop before using 30 days for your business. To do this debit your Expense account and credit your Prepaid Expense account. The money paid relates to a future accounting period. The expenses include gross salaries and liability accounts. The journal entries for prepaid rent are as follows. This creates a prepaid expense adjusting entry. Income must be recorded in the accounting period in which it is earned. Journal Entry for Salary Paid in Advance. Salary paid in advance is also known as prepaid salary it is a prepaid expense.

For example you have paid one month advance rent of your business shop before using 30 days for your business. Prepaid expense acts like an asset and. The adjusting entry at the end of January to reflect the rent expense of 5000 for that month. To do this debit your Expense account and credit your Prepaid Expense account. These are all entered as a Credit in your payroll journal. Journal Entries of Prepaid Expenses Prepaid expenses are those which are paid but whose service has not obtained from service provider. Initial journal entry for prepaid rent. Advance Salary Paid For the Month At the end of accounting period when the company actually receives the services then Prepaid Salary Account is. This creates a prepaid expense adjusting entry. In addition to the salaries recorded above the company has incurred additional expenses pertaining to the salaried payroll for this semi-monthly period of December 1631.

Cash Bank ac XXX. Primary Payroll Journal Entry The primary journal entry for payroll is the summary-level entry that is compiled from the payroll register and which is recorded in either the payroll journal or the general ledger. To record the salaries and withholdings for the work period of December 16-31 that will be paid on December 31. Salaried Payroll Entry 1. This one month advance rent will be prepaid expense. Prepaid expense acts like an asset and. Prepaid expenses are payments made in advance resulting into a right to receive compensation or a claim to use assets of another entity like prepaid insurance and prepaid rent. Payroll Journal Entries Payroll accounting is recording of salary expenses into the general ledger. Income must be recorded in the accounting period in which it is earned. Your journal entry reflecting the actual expense should look like this.

Salaried Payroll Entry 1. 5000 Prepaid salary is debited because we have paid in advance so it is our asset and assets have dr balance. Salary paid in advance is also known as prepaid salary it is a prepaid expense. For example you have paid one month advance rent of your business shop before using 30 days for your business. Prepaid income is revenue received in advance but which is not yet earned. To do this debit your Expense account and credit your Prepaid Expense account. This creates a prepaid expense adjusting entry. These are expenses but taken as an asset because the benefit from them is still due. Prepaid expense acts like an asset and. Cash Bank ac XXX.

Income must be recorded in the accounting period in which it is earned. The expenses include gross salaries and liability accounts. Cash Bank ac XXX. To record the payment of cash which created the prepaid expense the accounting records will show the following bookkeeping entries on 1 January. Journal Entry for Salary Paid in Advance. The journal entry would be as follows. This entry usually includes debits for the direct labor. To do this debit your Expense account and credit your Prepaid Expense account. The adjusting entry at the end of January to reflect the rent expense of 5000 for that month. The liabilities include income tax payable and payroll taxes payable accounts etc.