Awesome Ifrs For Smes 2018 Profitability Ratio Interpretation

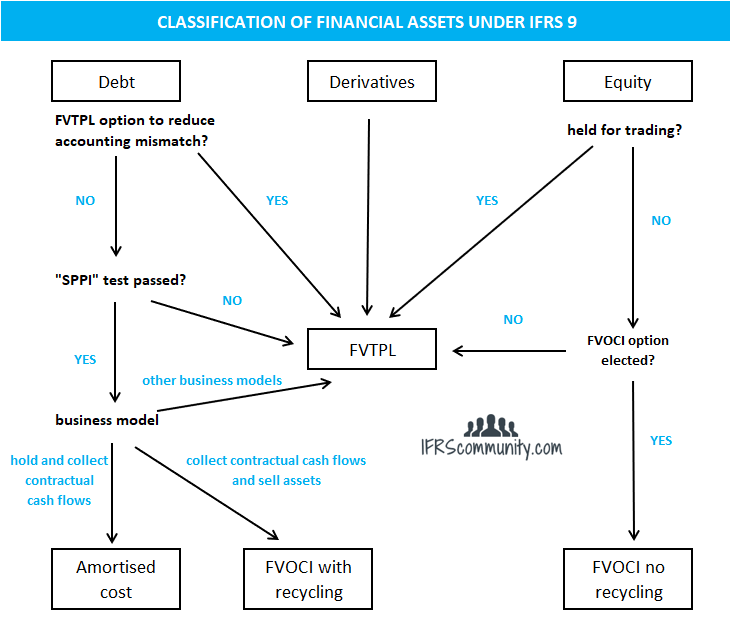

Classification Of Financial Assets Liabilities Ifrs 9 Ifrscommunity Com

IFRS for SMEs Standard translationsstatus report. P10 The term small and medium-sized entities as used by the IASB is defined and explained in Section 1 Small and Medium-sized Entities. IFRS for SMEs Standardcomprehensive review. Standard for Small and Medium-sized Entities IFRS for SMEs. The IFRS for SMEs Update is a staff update about news relating to the International Financial Reporting Standard for Small and Medium-sized Entities IFRS for SMEs Standard. 33 An entity whose financial statements comply with the IFRS for SMEs shall make an explicit and unreserved statement of such compliance in the notes. USE OF IFRS FOR SMEs- PUBLICALLY ACCOUNTABLE ENTITIES USE OFIFRS FOR SMEs- PARENT IS A FULL IFRS If a publicly accountable entity uses the IFRS for SMEs its financial statementsshall not be described as conforming with the IFRS for SMEs. Where it states Similar to IFRS for SMEs this means that the guidance is not identical and there are minor differences. It is based on IFRS Standards with modifications to reflect the needs of users of SMEs financial statements and cost-benefit considerations. International Financial Reporting Standards IFRS.

IFRS for SMEs Standard translationsstatus report.

This Update includes information on. The alternative and simplified version of full IFRS - Effective from January 2018. The SMEs Standard is self-contained incorporating accounting principles based on extant IFRS Standards which have been simplified to suit the entities that fall within its scope. View this and all previous IFRS for SMEs Updates here. IFRS for SMEs applies to all entities that do not have public accountability. The June 2018 IFRS for SMEs Update is now available.

IFRS for SMEs Standardcomprehensive review. IFRS for SMEs Standard modules completed. The future of financial reporting for small medium size entities in Saudi Arabia. The IFRS for SMEs defines SMEs as entities that. 33 An entity whose financial statements comply with the IFRS for SMEs shall make an explicit and unreserved statement of such compliance in the notes. -250 pages Simplified IFRSs but built on an IFRS foundation Completely stand-alone Designed specifically for SMEs. This is even the case if law or regulation in the entitys jurisdiction permits or requires IFRS for SMEs to be. 30 June 2017 and effective on or after 1 January 2018 with the exception of IFRS 16 and IFRS 17. The Financial Reporting Faculty answers some frequently asked questions on the International Financial Reporting Standard for Small and Medium-sized Entities IFRS for SMEs covering which entities are eligible to use the IFRS for SMEs the benefits of using the IFRS for SMEs and some of the key differences to full IFRSs. IFRS for SMEs Standard held at the Ministry of Finance of Georgia.

The IFRS for SMEs Standard is intended for entities that are not publicly accountable and publish general-purpose financial statements for external users. -250 pages Simplified IFRSs but built on an IFRS foundation Completely stand-alone Designed specifically for SMEs. USE OF IFRS FOR SMEs- PUBLICALLY ACCOUNTABLE ENTITIES USE OFIFRS FOR SMEs- PARENT IS A FULL IFRS If a publicly accountable entity uses the IFRS for SMEs its financial statementsshall not be described as conforming with the IFRS for SMEs. Update on IFRS for SMEs Standard modules. IFRS for SMEs Standardcomprehensive review. View this and all previous IFRS for SMEs Updates here. It is based on IFRS Standards with modifications to reflect the needs of users of SMEs financial statements and cost-benefit considerations. Companies applying IFRS for SMEs will have the opportunity to prepare their financial statements using a set of standards based on the truly global financial reporting language. The IFRS for SMEs 6 Good Financial Reporting Made Simple. Standard for Small and Medium-sized Entities IFRS for SMEs.

The alternative and simplified version of full IFRS - Effective from January 2018. Companies applying IFRS for SMEs will have the opportunity to prepare their financial statements using a set of standards based on the truly global financial reporting language. This is even the case if law or regulation in the entitys jurisdiction permits or requires IFRS for SMEs to be. -250 pages Simplified IFRSs but built on an IFRS foundation Completely stand-alone Designed specifically for SMEs. The Update is published on a regular basis with news about adoptions resources and implementation guidance. The future of financial reporting for small medium size entities in Saudi Arabia. The Financial Reporting Faculty answers some frequently asked questions on the International Financial Reporting Standard for Small and Medium-sized Entities IFRS for SMEs covering which entities are eligible to use the IFRS for SMEs the benefits of using the IFRS for SMEs and some of the key differences to full IFRSs. It is based on IFRS Standards with modifications to reflect the needs of users of SMEs financial statements and cost-benefit considerations. Financial statements shall not be described as complying with the IFRS for SMEs unless they comply with all the requirements of this Standard. IFRS for SMEs Standard translationsstatus report.

IFRS for SMEs Standardcomprehensive review. View this and all previous IFRS for SMEs Updates here. An entity has public accountability if it files its financial statements with a securities. A Do not have public accountability and b Publish general purpose financial statements for external users and paragraph 15 of the standard states that if a publicly accountable entity uses the IFRS for SMEs its financial statements shall not be described as conforming to the IFRS for SMEs. IFRS for SMEs Standard translationsstatus report. This Update includes information on. The Accounting Standards Board of Papua New Guinea ASBPNG has approved the IFRS for SMEs Standard for use by entities without public accountability in Papua New Guinea effective for accounting periods beginning on or after 1 January 2018. There are a number of accounting standards and disclosures that may not be relevant for the users of SME financial statements. The April 2019 IFRS for SMEs Update is now available. IFRS for SMEs Standard held at the Ministry of Finance of Georgia.

International Financial Reporting Standards IFRS. Where this publication states Same as IFRS for SMEs this means that the IASB guidance is identical in full IFRS as IFRS for SMEs. The IFRS for SMEs is based on full IFRS with modifications to reflect the needs of users of SMEs financial statements and cost-benefit considerations. Compliance with the IFRS for SMEs. P10 The term small and medium-sized entities as used by the IASB is defined and explained in Section 1 Small and Medium-sized Entities. The April 2019 IFRS for SMEs Update is now available. IFRS Foundation issues supporting materials for the IFRS for SMEs Standard The IFRS Foundation has issued three standalone educational modules that support the learning. IFRS for SMEs applies to all entities that do not have public accountability. Where it states Similar to IFRS for SMEs this means that the guidance is not identical and there are minor differences. The alternative and simplified version of full IFRS - Effective from January 2018.