Great Debit And Credit Side Of Trial Balance Ratio Analysis A Tool Financial Statement

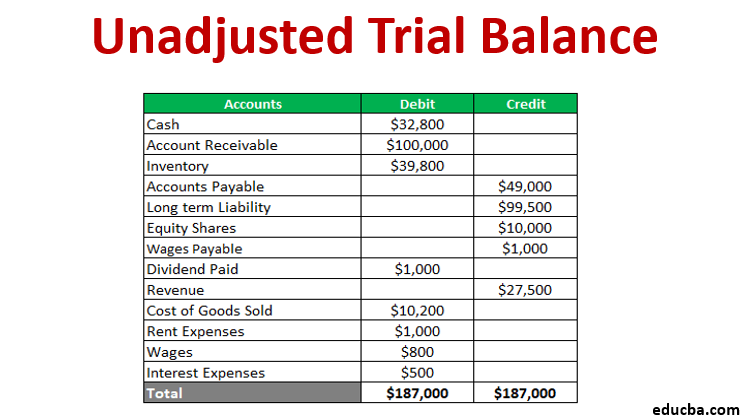

Unadjusted Trial Balance Format Uses Steps And Example

In such case the difference in trial balance is transferred to a. The ledger balances ie of all expenses incomes receipts payments assets liabilities share premiums etc. Debits include accounts such as asset accounts and expense accounts. We can see everything clearly and make sure it all balances. If all accounting entries are recorded correctly and all the ledger balances are accurately extracted the total of all debit balances appearing in the trial balance must equal to the sum of all credit balances. If totals are not equal it means that an error was made in the recording andor posting process and should be investigated. The trial balance is a bookkeeping systematized worksheet containing the closing balances of all the accounts. Trial Balance is required to prepare Financial statements profit loss account and Balance Sheet. It is prepared periodically usually while reporting the financial statements. Prepare a trial balance dated September 30.

The trial balance is used to test the equality between total debits and total credits.

Thanks for the A2A Mohini Gupta Trial Balance is prepared to check the accuracy of our accounts. Hence the balance of the discount received account is shown on the credit side. There are two sides of it- the left-hand side Debit and the right-hand side Credit. A trial balance is a conglomerate of or list of debit and credit balances extracted from various accounts in the ledger including cash and bank balances from cash book. Thanks for the A2A Mohini Gupta Trial Balance is prepared to check the accuracy of our accounts. For every debit there will be a credit and vice-versa.

Trial Balance shows the ledger balances of all the accounts. The ledger balances ie of all expenses incomes receipts payments assets liabilities share premiums etc. Are to be reported in the trial balance. The trial balance has two sides the debit side and the credit side. There are two sides of it- the left-hand side Debit and the right-hand side Credit. The trial balance is a bookkeeping systematized worksheet containing the closing balances of all the accounts. But due to some clerical error done while doing the accounting there are chances that trial balance will not agree. In such situation trial balance must be tallied. All debit accounts are meant to be entered on the left side of a ledger while the credits on the right side. Debit side of trial balance include- opening stock Purchase Sales return Depreciation All expenses discount AllowedInterest paid Bad debts insurance premiumetc All assets including cashbankdebtorsetc.

Debit side of trial balance include- opening stock Purchase Sales return Depreciation All expenses discount AllowedInterest paid Bad debts insurance premiumetc All assets including cashbankdebtorsetc. Prepare a statement of owners equity for month ending September 30 20. Asset and expense accounts appear on the debit side of the trial balance whereas liabilities capital and income accounts appear on the credit side. A trial balance is the accounting equation of our business laid out in detail. Debits include accounts such as asset accounts and expense accounts. It will be affected by double the amount. T Accounts Debits and Credits Trial Balance and Financial Statements. It has our assets expenses and drawings on the left the debit side and our liabilities revenue and owners equity on the right the credit side. The totals of these two sides should be equal. It shows a list of all accounts and their balances either under the debit column or credit column.

There are two sides of it- the left-hand side Debit and the right-hand side Credit. Writing the balance of an account on the wrong side of the Trial Balance. T Accounts Debits and Credits Trial Balance and Financial Statements. A trial balance is a list of the balances of all of a businesss general ledger accounts. Debits include accounts such as asset accounts and expense accounts. The rule to prepare trial balance is that the total of the debit balances and credit balances extracted from the ledger must tally. It is prepared periodically usually while reporting the financial statements. In such case the difference in trial balance is transferred to a. But due to some clerical error done while doing the accounting there are chances that trial balance will not agree. Asset and expense accounts appear on the debit side of the trial balance whereas liabilities capital and income accounts appear on the credit side.

In such situation trial balance must be tallied. A credit increases the balance of a liabilities account and a debit decreases it. The rule to prepare trial balance is that the total of the debit balances and credit balances extracted from the ledger must tally. Prepare an income statement for month ending September 30 20. A trial balance is a list of the balances of all of a businesss general ledger accounts. Are to be reported in the trial balance. Generally capital revenue and liabilities have credit balance so they are placed on the credit side of trial balance. The debit and credit side of the trial balance should be equal. The debit side and the credit side must balance meaning the value of the debits should equal the value of the credits. Prepare a statement of owners equity for month ending September 30 20.

Hence the balance of the discount received account is shown on the credit side. The debit side and the credit side must balance meaning the value of the debits should equal the value of the credits. Asset and expense accounts appear on the debit side of the trial balance whereas liabilities capital and income accounts appear on the credit side. Are to be reported in the trial balance. Items that appear on the credit side of trial balance. The trial balance has two sides the debit side and the credit side. In such case the difference in trial balance is transferred to a. Trial Balance shows the ledger balances of all the accounts. For every debit there will be a credit and vice-versa. Debits include accounts such as asset accounts and expense accounts.