Cool Ias 7 Cash And Equivalents Robinhood Income Statement

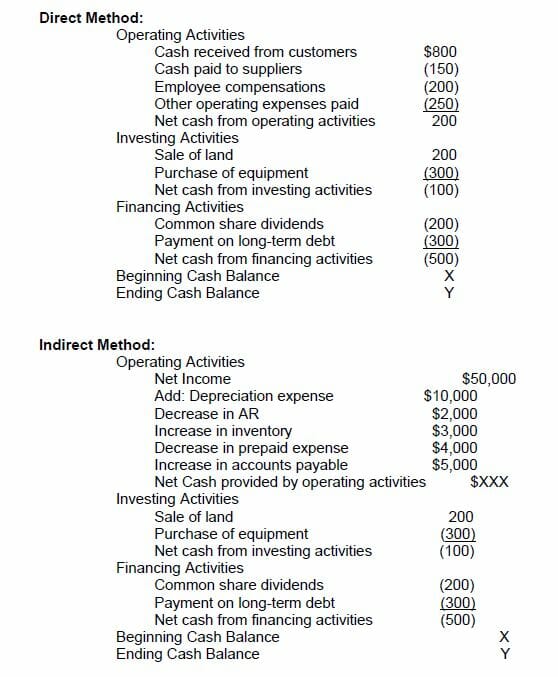

Statement Of Cash Flows How To Prepare Cash Flow Statements

Under IAS 7 cash flows are classified into operating investing and financing activities in a manner which is most appropriate to its business IAS 710-11. Find articles books and online resources providing quick links to the standard summaries guidance and news of recent developments. Cash equivalents are short-term highly liquid investments that are readily convertible to known amounts of cash and that are subject to an insignificant risk of changes in value. Investing activities are the acquisition and disposal of long-term assets and other investments not included in cash equivalents. If the two numbers were always the same then IAS 7 has a redundant paragraph 45 requiring a reconciliation between cash and cash equivalents in the statement of cash flows and the equivalent in the SOFP. This is because even though IAS 7 permits offset of balances in the statement of cash flows this may not be permitted by IAS 32 Financial Instruments. IAS 7 is to require entities to report their historical changes in cash and cash equivalents by means of a Statement of Cash Flows which classifies the periods cash flows by operating investing and financing. 1 can be immediately exchange for known amount 2 very close to maturity maximum 3 months Cash and cash equivalents are recognised as a. However care is required when presenting bank overdrafts and cash and cash equivalents in the statement of financial position. 45 An entity shall disclose the components of cash and cash equivalents and shall present a reconciliation of the amounts in its statement of cash flows with the equivalent items reported in the statement of financial position.

Statement of cash flows The accounting standard IAS 7 requires reporting entities to present information about historical changes in cash and cash equivalents through cash flow statements.

IAS 7 Cash Flow -Cash cash and bank accounts. Cash equivalents are investments that are IAS 76-9. Cash is defined by IAS 7 as cash on hand and demand deposits. Cash flows are inflows and outflows of cash and cash equivalents. 45 An entity shall disclose the components of cash and cash equivalents and shall present a reconciliation of the amounts in its statement of cash flows with the equivalent items reported in the statement of financial position. Cash equivalents are short-term highly liquid investments that are readily convertible to known amounts of cash and that are subject to an insignificant risk of changes in value.

45 An entity shall disclose the components of cash and cash equivalents and shall present a reconciliation of the amounts in its statement of cash flows with the equivalent items reported in the statement of financial position. However care is required when presenting bank overdrafts and cash and cash equivalents in the statement of financial position. If the two numbers were always the same then IAS 7 has a redundant paragraph 45 requiring a reconciliation between cash and cash equivalents in the statement of cash flows and the equivalent in the SOFP. The objective of IAS 7 is to require the presentation of information about the historical changes in cash and cash equivalents of an entity by means of a statement of cash flows which classifies cash flows during the period according to operating investing and financing activities. This is because they are essentially equity instruments that have no maturity. Under IAS 7 cash flows are classified into operating investing and financing activities in a manner which is most appropriate to its business IAS 710-11. There are reasons why the two numbers may not be the same and the explanation hinges around what the entity has defined as cash and cash equivalents in its statement. IAS 7 para 6. Held for meeting short-term cash commitments. The objective of IAS 7 is to require the presentation of information about the historical changes in cash and cash equivalents of an entity by means of a statement of cash flows which classifies cash flows during the period according to operating investing and financing activities.

IAS 7 defines cash equivalents as short-term highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. IAS 7 Cash flows are inflows and outflows of cash and cash equivalents. IAS 7 para 6. Operating activities are the principal revenue-producing activities of the entity and other activities that are not investing or financing activities. Cash equivalents are short-term highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. IAS 7 Components of cash and cash equivalents. Under IAS 7 cash flows are classified into operating investing and financing activities in a manner which is most appropriate to its business IAS 710-11. Cash and cash equivalents include unrestricted cash meaning cash actually on hand or bank balances whose immediate use is determined by the management other demand deposits and short-term. The objective of IAS 7 is to require the presentation of information about the historical changes in cash and cash equivalents of an entity by means of a statement of cash flows which classifies cash flows during the period according to operating investing and financing activities. IAS 7 Cash Flow -Cash cash and bank accounts.

IAS 7 prescribes how to present information in a statement of cash flows about how an entitys cash and cash equivalents changed during the period. The objective of IAS 7 is to require the presentation of information about the historical changes in cash and cash equivalents of an entity by means of a statement of cash flows which classifies cash flows during the period according to operating investing and financing activities. IAS 7 Determination of cash equivalents Date recorded. Cash and cash equivalents include unrestricted cash meaning cash actually on hand or bank balances whose immediate use is determined by the management other demand deposits and short-term. There are reasons why the two numbers may not be the same and the explanation hinges around what the entity has defined as cash and cash equivalents in its statement. IAS 7 defines cash equivalents as short-term highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. Cash is defined by IAS 7 as cash on hand and demand deposits. This is because even though IAS 7 permits offset of balances in the statement of cash flows this may not be permitted by IAS 32 Financial Instruments. Operating activities are the principal revenue-producing activities of the entity and other activities that are not investing or financing activities. Cash and cash equivalents Definition of cash and cash equivalents.

Cash equivalents are short-term highly liquid investments that are readily convertible to known amounts of cash and that are subject to an insignificant risk of changes in value. The definition of cash equivalents makes reference to them being both highly liquid and subject to an insignificant risk of changes in value. Find articles books and online resources providing quick links to the standard summaries guidance and news of recent developments. The objective of IAS 7 is to require the presentation of information about the historical changes in cash and cash equivalents of an entity by means of a statement of cash flows which classifies cash flows during the period according to operating investing and financing activities. IAS 7 Components of cash and cash equivalents. CASH AND CASH EQUIVALENTS Short term wherethe original maturityis 3 months or lessirrespectiveof timingpost balancedate Highlyliquid investments Readily convertibletoknown amounts of cash Subject to insignificantriskof changes invalue. IAS 7 Statement of cash flows. This is because even though IAS 7 permits offset of balances in the statement of cash flows this may not be permitted by IAS 32 Financial Instruments. IAS 7 Cash flows are inflows and outflows of cash and cash equivalents. IAS 7 Cash Flow -Cash cash and bank accounts.

Cash equivalents are short-term highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. CONSIDERATIONS TO NOTE Non cash investing and financing activities must be disclosed. IAS 7 Cash Flow -Cash cash and bank accounts. 45 An entity shall disclose the components of cash and cash equivalents and shall present a reconciliation of the amounts in its statement of cash flows with the equivalent items reported in the statement of financial position. IAS 7 Cash flows are inflows and outflows of cash and cash equivalents. Held for meeting short-term cash commitments. IAS 7 Determination of cash equivalents Date recorded. Under IAS 7 cash flows are classified into operating investing and financing activities in a manner which is most appropriate to its business IAS 710-11. IAS 7 prescribes how to present information in a statement of cash flows about how an entitys cash and cash equivalents changed during the period. Find articles books and online resources providing quick links to the standard summaries guidance and news of recent developments.